Bitcoin Short-Term Holders Hit Record Loss Capitulation

What You Need to Know

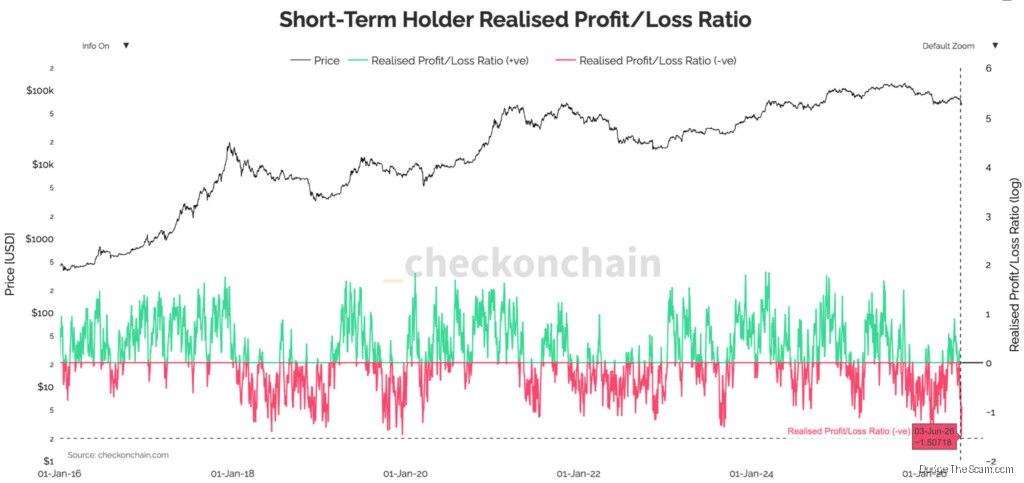

- Short-term Bitcoin holders locked in losses at unprecedented levels, with ratio hitting -1.5.

- 53,800 BTC moved to exchanges in 24 hours, all transferred at a loss this year.

- 10.5 million BTC now held at loss versus 9.8 million in profit, a historical crossover point.

- Bitcoin’s 2024 halving supply shock narrative facing macro headwinds since 2020.

Short-term Bitcoin holders are capitulating at a pace with no recorded precedent. The Short-Term Holder Realized Profit/Loss Ratio tracked by CheckOnChain has hit -1.5, meaning losses being locked in by holders of under 155 days are overwhelming any remaining profit in that cohort by a margin deeper than any prior reading in the dataset.

The on-chain picture compounds that signal. CryptoQuant data captured roughly 53,800 BTC moving from short-term holders onto exchanges within a single 24-hour window, with every coin in that batch transferred at a loss, the most lopsided such flow recorded this year. Coins moving to exchanges carry an implied intent to sell, so the two metrics together describe the same phenomenon from different angles: a cohort that bought during the post-halving run-up is now exiting, largely in the red, and doing so in size. The Fear and Greed Index sitting at 12 reflects that mood, though sentiment readings tend to lag behavior rather than lead it. What matters more is that the 2024 halving’s supply shock narrative, which historically takes six to twelve months to materially affect price, has been running directly into macro headwinds that Bitcoin has tracked closely since 2020.

Glassnode shows 10.5 million BTC now held at a loss against 9.8 million in profit, a crossover that has coincided with major bottoms in prior cycles, though coincidence and causation are worth keeping separate here.

Who Is on the Other Side

The relevant question is not whether this looks like capitulation, it does, but whether the buyer base has changed enough across cycles to make the historical pattern reliable. In 2022, capitulation events were absorbed slowly and unevenly, with retail largely absent and institutional infrastructure still immature. Spot ETFs now exist, and sustained institutional inflows could accelerate the transfer from distressed short-term sellers to longer-duration holders faster than prior cycles allowed. The counter-risk is that ETF flows have themselves shown sensitivity to macro sentiment, and if equity markets continue softening under rate pressure, the institutional bid is not unconditional. Bitcoin retracing to the 200-week moving average is a real data point, not a talking point; that level has acted as support in every prior bear market, but the current drawdown of roughly 50% from the October high is within the range of corrections seen during bull markets, not exclusively bear ones.

The setup is coherent. Distressed supply is moving, long-term holders are not, and price is sitting at a level that has historically mattered. Whether that translates into a floor depends almost entirely on the composition and conviction of whoever is absorbing these coins, and that answer will show up in exchange outflow data before it shows up anywhere else.

0 Comments